III.2. Communication of CSR

Franzisca Weder

The lady…

In the previous chapters, CSR communication was identified as “process of anticipation stakeholder’s expectations, articulation of CSR policy and managing different tools designed to provide true and transparent information about a company’s or a brand’s integration of its business operations, social and environmental concerns, and interactions with stakeholders” (Podnar, 2008).

This includes marketing communication and public relations, promoting a certain product with communication focused on the transmission of information. As such, Coca Cola informs their customers in a one-directional manner – in my case about their bottles being made out of recycled plastic, at least to a certain percentage. This is one example of communication of a certain aspect of sustainability related to the big problem of plastic waste, pollution of the oceans and challenges around recycling. Furthermore, Coca Cola communicate that they “act in ways to create a more sustainable and better shared future. To make a difference in people’s lives, communities and our planet by doing business the right way” (Coca Cola, 2023). Product information, advertising and marketing as much as website information and reporting are part of communication of sustainability, as defined in the scheme below.

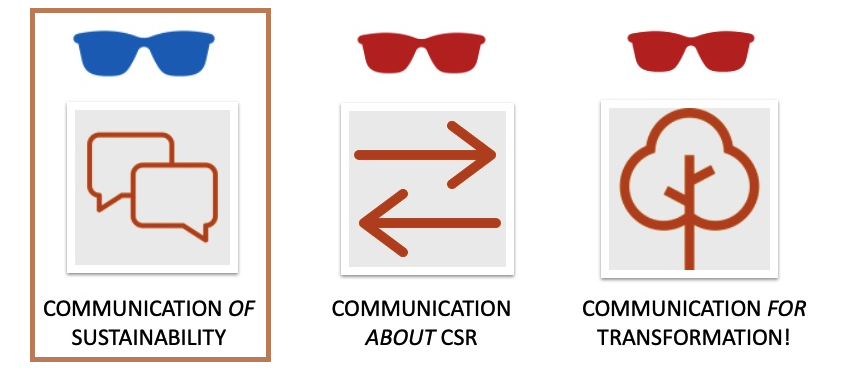

Image: “Dimensions of Sustainability Communication” by Franzisca Weder

In brief, communication of CSR related activities and an organization’s understanding of sustainability and sustainable development is characterized by the following mode of communication and function:

Communication of CSR / sustainability

Direction / mode of communication:

One-directional, transmissive, sender-receiver, one to many

Function:

Transmission, information and knowledge transfer towards an objective

Communication of CSR and sustainability is therefore sender and communicator oriented. Academic research is studying corporations, political institutions but also civil society organizations and Nonprofits and asks for their vision, goals and key messages, how they communicate and what the channels are that are used (social media against traditional media, reporting, see below, etc.). Communication professionals and consultants develop strategies and best practice frameworks for the communication of CSR activities, projects and corporate goals.

CSR campaigning and communication of CSR

The most established understanding of communication is that information can be transmitted and disseminated towards a specific target audience or more general: a ‘receiver’ of the information. Communication fulfills a certain purpose, it is used and thus a tool to achieve the communicator’s objectives and thus can be monitored in terms of its effects (for example: reputation gain).

Communication of CSR happens mostly in form of a so called ‘campaign’, which is a connected series of operations designed to bring about a particular result. A campaign includes communication processes on an interpersonal, group, and organizational level but focuses mostly on media and public relations. Internal and external communication processes are integrated (If you want to learn more about campaigning, watch the recorded lecture, Campaigning (YouTube, 17m5s)). Campaigns can be differentiated in regard to their timeframe and scope, so they are either focused on a short-term, mid-term or long-term goal and either conceptualized as information, awareness or behavior change campaign.

These specific communication activities can be explained with a more detailed look at various ‘senders’ of CSR related information, or ‘communicators’ in the field of CSR communication:

As said, Civil Society organizations develop and implement information campaigns that are conceptualized in a similar way compared to marketing: the main goal is to reach awareness for the organization and inform a wider public about the main purpose and related activities. One example is the World Health Organization (WHO) which has the following goal:

“Raising awareness and thereby understanding of the effects of climate change on health will facilitate both behavioural change and societal support for the actions needed to reduce greenhouse gas emissions. It can also help in getting health-care professionals to support strategies for mitigation and adaptation that will both improve health and reduce vulnerability” (WHO, 2023).

WHO/Europe is implementing a broad range of activities on climate change and health. They include advocacy campaigns and multimedia products addressing both policy-makers and the general public; a comprehensive set of policy briefs, guidance, tools and training manuals; and engagement in climate fora to raise the prominence of health issues on the climate agenda.”

Very similar, education institutions seek to inform their key stakeholders, students and staff, but also the community of alumni and future students for example about their activities in the areas of diversity management and inclusion, greening the campus of gender sensitivity. The activities reach from climate change and sustainability related research clusters to on campus events that are sustainability certified, and it also includes recycling systems or water refill-stations. The strategic goals is to transfer facts in and beyond classroom settings. One example is The University of Queensland in Brisbane, Australia, which developed a Sustainability Strategy, with the following goal:

“Action plans to deliver on the commitments in the UQ Sustainability Strategy are being produced in collaboration with the relevant University areas. Our plans are designed to create a tangible path between where the University is now and where it seeks to be, across each focus topic.” (UQ Sustainability Strategy, n.d.).

One example for their communication of sustainability is the Warwick Solar Farm.

Photo by Red Zeppelin on Unsplash

Next to societal institutions in the education sector, even media corporations communicate about how they take responsibility and inform their audience – shareholders and target audiences – about their commitment to a more sustainable world and future. The BBC (UK) publishes the following commitment:

“Raising awareness and thereby understanding of the effects of climate change on health will facilitate both behavioural change and societal support for the actions needed to reduce greenhouse gas emissions.We can’t enhance our audiences’ understanding of climate change and what’s needed to transition to Net Zero unless we are also working on the solutions to reduce greenhouse gas (GHG) emissions within our own industry. As a publicly funded organisation, we understand that we have a particular responsibility in this area” (BBC, 2023).

One goal is for example to reduce the environmental impact of their programmes, or talking about sustainability on screen. Communication of sustainability thus includes environmental journalism, climate change reporting as well as documentaries but also the CSR activities as a business, from recycling to reduction of plastic waste.

Next to Universities or schools, scientific institutions, from museums to research institutions also transfer scientific results and facts for a better public understanding of science; the focus of the Frauenhofer Institute for example is to play a

“key role in anchoring the concept of sustainability in corporate policy and communication” (ISC, 2023).

Political institutions do not only work with civil society-actors and scientific institutions; ministries, parties, communities, and municipalities seek to inform the people, make people familiar with the political will of parties, the government and with the bureaucratic structures. One example is the European Union, which has been mentioned a couple of times in the CSR context. They communicate in a series of awareness campaigns with the following goal:

“This measure encompasses actions that promote awareness for the altered conditions under climate change and adaptation. However, not all stakeholders are aware and informed about their vulnerability and the measures they can take to pro-actively adapt to climate change. Awareness raising is therefore an important component of the adaptation process to manage the impacts of climate change, enhance adaptive capacity, and reduce overall vulnerability” (Climate ADAPT, n.d.).

At the forefront of communication of CSR are corporations and business, informing their stakeholders on possible behavior, their projects and strategies with the main goal to improve reputation. The main field of communication of CSR that follow this direction of information transfer is happening under the label of ‘corporate reporting‘ – mainly on websites, partly on social media, and definitely in official ‘non-financial’ reports. This is why we want to take a closer look at CSR reporting.

Corporate / CSR reporting

The first policy documents and mainly the Brundtland report (Hauff, 2007) (see chapter I.2) has stimulated the idea of non-financial reporting. Non-financial means an organization’s formal disclosure of information that is not related to finances, financial performance. Non-financial reporting focuses on issues and related activities in an environmental, social or governance dimensions (ESG, see also chapter I.2.). But is not only the CSR strategy that is communicated; CSR, Sustainability or ESG reporting includes measurable actions that an organization takes to tackle environmental problems.

As well, events like the BP Oil Spill or corporate scandals around child labour or working conditions in the garment industry after the burning factory in Bangladesh, have emphasized the importance of transparency and accountability in terms of being responsible towards the society – towards humans and nature. One reaction to those events is that stakeholders increasingly demand information on organization’s CSR performance – and allocate responsibility for ‘good’ behavior to corporates in particular. Thus, there is a growing need of ‘not only being socially responsible but also communicating this commitment to the stakeholders through corporate social responsibility reporting to enhance company’s reputation’ (Perez, 2015; Khan et al., 2020).

At the beginning, large and multinationally operations companies started to publish information on their products and services, their quality, equal opportunities and social benefits for the own employees and the companies social contribution to the communities and environments where they operated (Fifka, 2013), followed by the first non-financial information campaigns, brochures or websites and reports particularly labeled as Environmental Reports (Davis-Walling & Batterman, 1997; Halme-Huse, 1997; Buhr, 2002). However, in this first decade of reporting, they were often criticized as ‘exercise in public relations’ (Cerin, 2002) or ‘add on’ to annual financial reports. While environmental reporting was voluntary, it was mostly about gaining recognition, reputation and displaying awareness of a beginning ecological crisis.

This changed with the concepts of Corporate Citizenship and Corporate Social Responsibility in the 1990s, leading to a much deeper reflection about and thus organization of actions in the dimensions of responsibility (environmental and social next to economic), theoretically and philosophically supported by concepts and research in the area of business ethics and corporate communication.

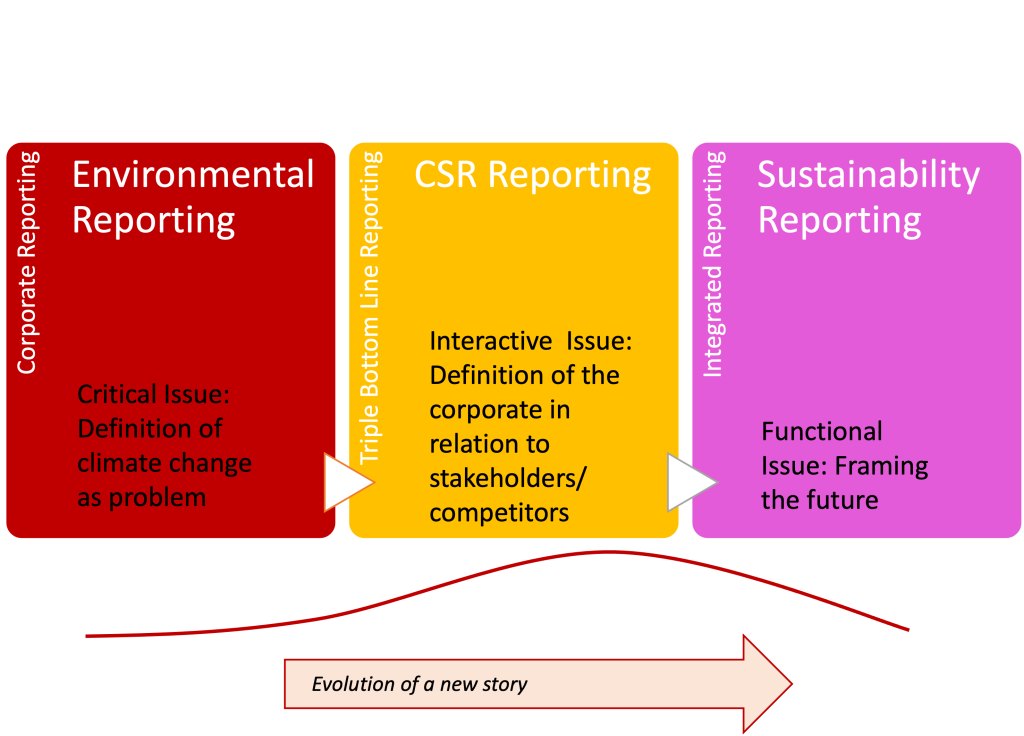

Image: “Development of non-financial reporting” by Franzisca Weder (adaption in Weder, 2023)

As the graph above show, now there is a decent body of knowledge around CSR communication (see again: Golob et al., 2013; Diehl et al., 2017; Weder et al., 2019) and CSR reporting in particular (overview in Khan et al. 2020), discussing expectations, impact, accountability, standardization and differences related to culture, size or organizational scope and beyond. CSR reporting dominated corporate communication from the mid 1990ies to 2005, where the first Corporate Sustainability Reports were published (Schaltegger et al., 2007; Hahn & Kühnen, 2013; Kolk, 2004; Buhr, 2010; Tschopp & Huefner, 2015).

Today, sustainability has become the dominating term that is used to describe the relationship between business and society, while CSR has become a more comprehensive term, a term that transformed from being predominantly related to internal business affairs to something that is now part of a broader societal discussion about sustainability (Aslaksen et al., 2021). This development has led to something new, something that is even broader from a terminological perspective, which is ‘ESG reporting’ (Bose, 2020) and new forms of presenting the sustainability narrative as Environmental & Social Governance. As defined in the terminological clean up in part I, the governance aspect includes the ‘agency’ that is taken for not only the organizational behavior but much more in regards to a certain problem that need to be tackled or public issue. So ESG is a concept that leads to strategic action in a specific issue area related to sustainable development the branch, industry and issues and organizations deals with. One example: LEGO can’t avoid that their product is made of plastic, but they can get engaged in an area, that their product links to and where they can legitimately take responsibility, i.e. in education – check their reporting.

As mentioned above, communication of CSR and sustainability is focused on information transfer; thus, CSR reporting helps the organizational stakeholders, in particular shareholders and thus investors, but also civil society organisations, consumers and other key audiences to evaluate the performance of companies with a sustainability and responsibility lense. This goes hand in hand with the development of frameworks for the reporting, especially current developments in Europe. For examples the EU law now requires all large / listed companies to disclose their risks and opportunities arising from social and environmental issues. The need to report their impacts of their activities on people and the environment. This new regulatory framework is part of the European green deal. To secure the measurability as well as comparability, there are new rules on corporate CSR and sustainability reporting, one key example is the Corporate Sustainability Reporting Directive.

The regulation also makes sense to give shareholders orientation and avoid greenwashing. The EU Taxonomie is a political way to support sustainable activities (in organizations / business with more than 500 employees) with a classification system that helps to clarify which investments are environmentally sustainable – in the context of the European Green Deal. The aim of the taxonomy is also to prevent greenwashing and to help investors make greener choices. In other countries, for example Australia, there is often no legal requirement for non-financial and ESG or sustainability reporting. However there are certain obligations on companies to report both financial and non-financial information in certain industries and areas.

A couple of ideas for practical reporting:

How to report?

What are the elements of a non-finial report?

- address the most relevant issues for the organization – negotiate the most relevant issues within your organization

- address the issues most pressing by the organization’s industry context and its shareholders – and include the local community; use primary & secondary research as well as consultation to uncover the priorities

- articulate a concrete goals for the year ahead

- develop SMART objectives and make clear commitments to achieving specific results, make your objectives measurable

- create a relationship between the actual and previous reports, showing what has improved in a company’s operation since its publication; by analyzing CSR reports, stakeholders should be able to track a company’s social responsibility journey

- publish and promote the report effectively; use various media environments – and again, create connections to current public issues, create communicative links;

- be accessible: the report should be accessible in terms of its style and how easily the key audiences can obtain it; but also be accessible in terms of the people who speak and represent the organization.

Structure of a report

- Business overview (provide context about the business, its people and the organizational environment)

- A letter from the CEO (create a key narrative, include personal reflections from the CEO, demonstrate leadership and commitment)

- A summary of progress (reference to previous reporting, progress made, objectives achieved)

- Goals (targets for improvement, based on short, mid and longterm goals)

- Sources and statistics (use references, use primary & secondary research, market data and existing reports and knowledge)

- Case studies (tell a story, use case studies, complementary to hard facts and data; explain challenges with detail)

- Contact information (be accountable and accessible).

What about evaluation?

Summary – most important take aways

Communication of CSR and sustainability is based on a pragmatic understanding of communication; communication is an instrument or tool that helps to inform the stakeholders and specific target audiences about CSR related activities and programs that an organization (predominantly corporations) put into place to take responsibility towards the society. The most elaborated form of communication of CSR is ‘CSR reporting’, ‘Sustainability reporting’ or, more recently, ‘ESG reporting’.

From a theoretical perspective, communication of CSR is mostly analyzed and explained with a focus on organizations and has thus a rather narrow perspective on CSR-related Public Relations and Marketing activities. Processes of social change and societal transformation processes are not necessarily included in models and concepts that are often developed with a specific goal and for application in communication and management practice. As well, sustainability is a language token used in CSR communication, but not further elaborated as a guiding principle of action on all levels, individual, organizational, social and ecological.

Finally, a lot of attention in research and (communication and consulting) practice is put on the formation of structures to institutionalize and stabilize CSR within organizations and the corporate world. This is expressed in an increasing number of resources (fundings, institutions, trainings etc.) as well as rules (policies and frameworks on national / supranational levels, reporting indices etc.).

In the next chapter, the ‘complement’ to organizational communication and communication of CSR, public discourses on CSR and the key role of the media will be further elaborated.

Further reading…

More academic literature on CSR reporting:

Aslaksen, H.M., Hildebrandt, C. & Johnsen, H.C.G. The long-term transformation of the concept of CSR: towards a more comprehensive emphasis on sustainability. Int J Corporate Soc Responsibility 6, 11 (2021). https://doi.org/10.1186/s40991-021-00063-9

Shabana, K. M., Buchholtz, A. K., & Carroll, A. B. (2017). The institutionalization of corporate social responsibility reporting. Business & Society, 56(8), 1107-1135.

Moravcikova, K., Stefanikova, Ľ., & Rypakova, M. (2015). CSR reporting as an important tool of CSR communication. Procedia Economics and finance, 26, 332-338.

Tschopp, D., & Huefner, R. J. (2015). Comparing the evolution of CSR reporting to that of financial reporting. Journal of business ethics, 127, 565-577.

Khan, M., Hassan, A., Harrison, C., & Tarbert, H. (2020). CSR reporting: A review of research and agenda for future research. Management Research Review, 43(11), 1395-1419.

Pollach, I. (2015). Strategic corporate social responsibility: The struggle for legitimacy and reputation. International Journal of Business Governance and Ethics, 10(1), 57-75.

Pollach, I., Johansen, T. S., Ellerup Nielsen, A., & Thomsen, C. (2012). The integration of CSR into corporate communication in large European companies. Journal of Communication Management, 16(2), 204-216.